There is little doubt that growing wealth and income inequality is a reality in the United States. Even in California we can see this microcosm unfold dramatically. You have people being pushed inland from coastal areas and those near employment hubs have seen housing values reach near peak levels. What we are also seeing is that access to debt is the key measure of success in this economy. For example, the bubble favorite ofinterest only loans is back but with a different flavor. Banks like Wells Fargo, Bank of America, and Union Bank are back at it underwriting interest only loans to wealthier clients. The big difference is that you need to have money to play in this current market. Banks are holding onto these loans in their own portfolios. Not a bad way to earn money in a low rate environment. So this hits at the heart of the issue where Fed policy has largely aided those least needing it in a modern day feudal banking network. For example, you can buy a $1,000,000 home today with a 3 year interest only mortgage and carry a principal and interest payment of $1,562 per month. Impossible? Welcome to the modern banking system where low rates are accessible to those who least need it.

Welcome back to interest only loans

Housing is already an incredibly subsidized industry. You have mortgage deductions, tax benefits, and essentially a hedge against inflation given that the Fed is set on digitally printing our way into prosperity. Access to debt is paramount in this system. The interest only mortgage is a perfect example of what happens when we create an artificially low rate interest environment.

“(LA Times) Bankers don’t seem worried about affluent clients missing payments. With high-end home prices on the rise, they have recently embraced jumbo mortgage lending, including interest-only mortgages. That trend continued this week as the banks reported earnings, with Bank of America Corp. saying 36% of its fourth-quarter mortgages were jumbo loans, up from 23% of originations in the first quarter.In a conference call with analysts Wednesday, BofA Chief Executive Brian Moynihan said the bank is making non-qualified mortgages to the rich and holding the loans as investments rather than selling them.“We’ll meet the needs of our customers by using our own balance sheet,” he said. “We do a lot of mortgages today through our wealth management business.”

Programs like this of course only add fuel to the flame of wealth inequality. Banks are willing to leverage virtually free money and lend it out to wealthy clients. Higher up on the food chain, you have Wall Street now crowding out regular buyers in the residential housing market. Over time this big money club gets more selective and the currency at play here is access to cheap money. Some would like to believe that this system is rewarding hard grit and free market success but in reality it is more reflective of cronyism in the financial sector (have people forgotten that most banks failed in utterly dramatic fashion and were bailed out Soviet style?). Nothing free market about that narrative. Give anyone access to large funds of money for nearly zero percent interest rates and see how many takers you will get. In a way, the first round of the housing bubble was this and we saw what unfolded when accessible to the general public. Today, the doors to the public have slammed shut and now access to debt is more selective.

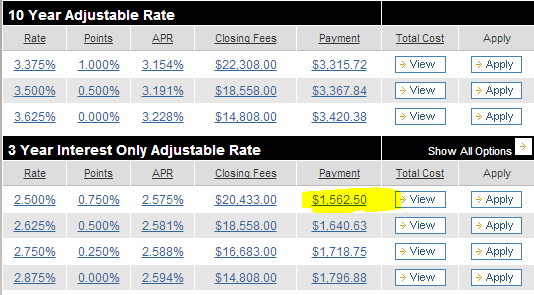

For example, let us assume we wanted to buy a $1 million home somewhere in California. We will put 25 percent down. How low can we make our monthly payment?

Assumptions: $1,000,000 home purchase, $250,000 down payment, FICO 740 and higher

An interest only loan for $750,000 (you still need 25 percent down) will cost us $1,562 per month (principal and interest) and we are nicely locked in for three years. Assume taxes and insurance run $1,000 per month and your monthly nut on a $1,000,000 home is $2,562. A similar rental may run $4,000 to $5,000 assuming many rentals are available in the area. So you are actually saving money here on a monthly basis on a big bet. Since many people believe that real estate will only move in one direction, after a few years and some appreciation, you just sell the place or refinance and off you go. Also, many are looking for those juicy deductions:

“Customers for such loans are often self-employed and capable of making big down payments and maintaining fat bank accounts. Banks believe such borrowers could afford traditional loans but want to maximize the cash available for other investments or ventures. Some borrowers just want the tax deduction available on the first $1 million a year in mortgage interest payments.”

Given that only 1 out of 3 families in California can actually afford a home, this low rate environment is creating big incentives for people that largely don’t need it. It shouldn’t come as a shock that million dollar home sales are now back to levels last seen near the peak of the last housing bubble in 2006:

You can understand why big money is crowding into real estate when low rates are providing such generous returns. The above scenario doesn’t factor in the tax breaks you will get which are important for higher income households. The interest rate on the 3 year interest only loan is 2.5 percent but for the regular Joe and Sally looking at more traditional products, the current rate is as follows:

The 30-year fixed rate mortgage is at 4.34 percent, nearly 200 basis points higher than the 3 year interest only loan. This is a tiny niche market here but products like this fueled by QE addiction are merely speeding up the wealth divide in the country. Borrowing your way into millionaire status doesn’t seem like a late night infomercial catch phrase anymore.

via:http://www.doctorhousingbubble.com/interest-only-loans-california-arms-interest-only-mortgages/?utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+DrHousingBubble-HowILearnedToLoveSocal+%28Dr.+Housing+Bubble+-+How+I+learned+to+Love+SoCal%29

No comments:

Post a Comment