Making homes unaffordable to younger Americans is more problematic than simply altering the living habits of upcoming generations. Housing formation in the United States is entering uncharted territory based on demographic shifts and also the new reality that younger Americans will be less affluent than their parents. This is why we have millions ofyounger Americans living at home with parents. Some may not view this as an issue but in the past, construction was a big part of GDP and you will have a hard time justifying new housing construction if people are simply living at home or are only able to afford a rental. The student debt crisis goes hand and hand with the unaffordable nature of housing for young Americans. It also doesn’t help that Wall Street is crowding out regular buyers in the market. With a growing population and investors eating up the low supply of housing, many young Americans are essentially in the position to move back home or to rent. Buying is a remote possibility for many Americans and this has put a clamp on new housing formation.

Household formation

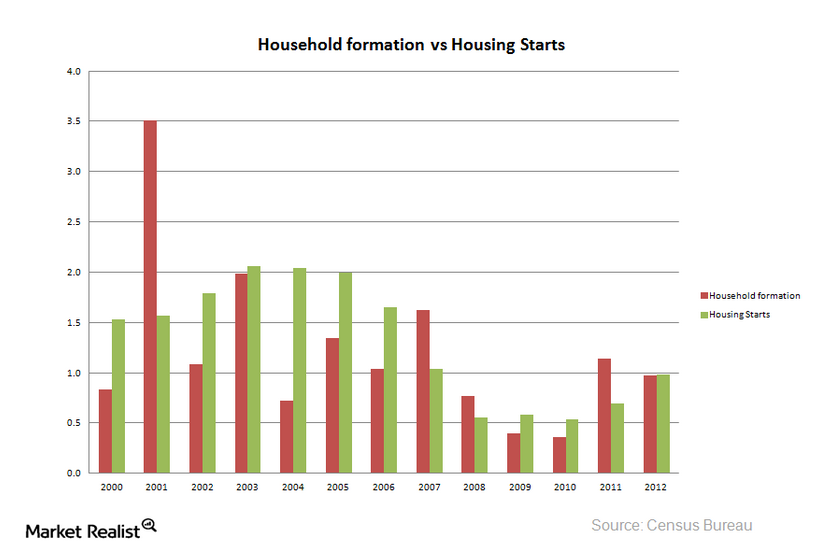

In stable markets you would expect that housing starts and household formation would track closely to one another. Builders can predict (to a certain degree) how many homes to build for upcoming families based on demographics. Yet this becomes difficult to predict when a large portion of those coming up are simply unable to afford a property. In the early 2000s toxic mortgages and no due diligence allowed anyone with a desire to buy to do so. So of course, when we look at household formation early in the decade we find that formation was far outstripping housing starts. If the bank is offering you crazy amounts of money for a nice place why would you say no? The bank is looking out for my interest right? At least that with greed mixed in led to the biggest housing bubble of all-time.

Here is a chart of both household formation and housing starts:

You’ll notice that between 2001 and 2002 builders got the message quickly and started building. In 2003 they nailed it in terms of demand and supply. However, from 2004 to 2006 there was a glut of overbuilding. In 2007 a tipping point occurred. Household formation was still high since the bubble didn’t pop late in the year but builders were already tapped out. From 2008 to 2010 household formation and building collapsed. In 2011 things have rebounded and in 2012 an equilibrium was struck. 2013 is the year investors devoured the market completely. Yet we need to remember that from 2008 to the present, the dominant market mover came in the form of investors. Driving up prices with no real increase in income forced many young Americans back home with mom and dad:

]

]

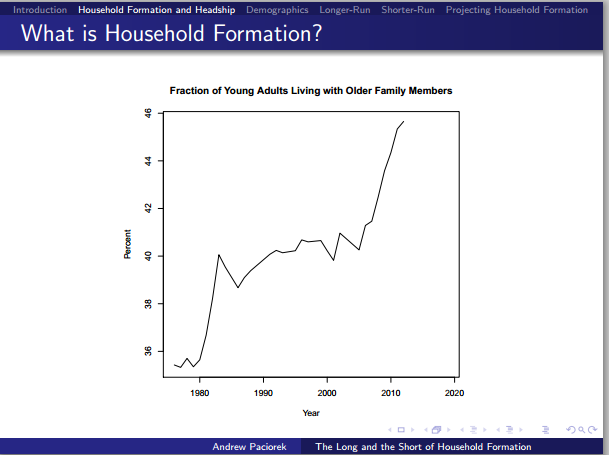

We have a dramatically high number of adults living at home seemingly during an economic recovery. Remember the recession has been officially over for nearly half a decade. Why do we continue to see a massive number of young adults living at home?

What is interesting is that this trend for the young is not new. It actually has been on-going for many years:

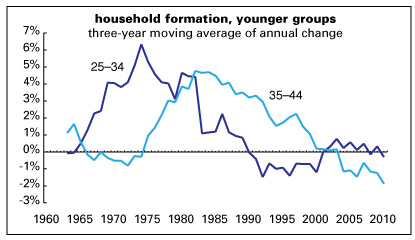

The trend is rather clear for those in the 25-34 age group and the 35-44 age group. What is going on is that more Americans are going to college but at the same time are also accumulating high levels of debt for jobs that essentially pay what they did decades ago adjusting for inflation (and less in many cases). Why is this important? Well even one generation ago, if someone picked the wrong major they at least were off in the market with little to no student debt. Today, pick the wrong major and you still have a good portion of your income going to student debt payments. This matters when your income is low.

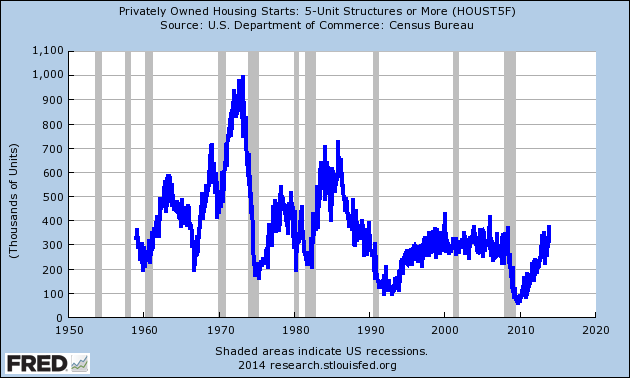

Builders realize that the nation is becoming one where more people will be renters out of economic necessity so multi-unit housing starts (i.e., apartments) are now going back up:

This is a fairly smart move for builders. Household formation will resume but it is highly doubtful that these people will be in the market for the more expensive McMansions given their incomes. Also, many are having a hard time contenting with the hot money flowing out of Wall Street into residential real estate.

The projections are clear, household formation will stabilize but housing will unlikely be a giant player in making our economy boom again:

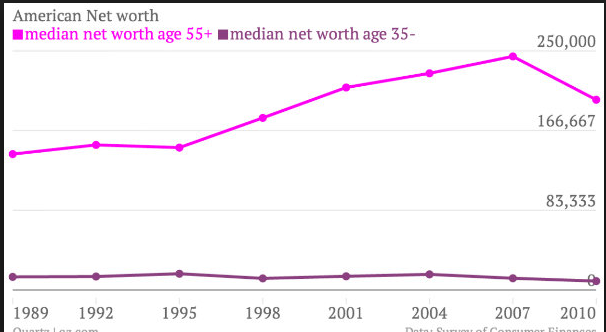

So it becomes apparent. After all, if you were a builder what motivation would you have to try to capture the attention of an audience with a median net worth of close to zero dollars. Older Americans, many who already own, are not in the market for new homes:

Then you wonder why we have millions of young Americans living with mom and dad and deep in student debt.

via:http://www.doctorhousingbubble.com/broke-young-and-unable-to-afford-a-home/?utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+DrHousingBubble-HowILearnedToLoveSocal+%28Dr.+Housing+Bubble+-+How+I+learned+to+Love+SoCal%29

No comments:

Post a Comment