While the stock market can turn on a dime with the agility of a cheetah, the housing market has the nimbleness of the Titanic. That is why the slowdown that started in the summer of 2013 is actually now resulting in on the ground changes for buyers and sellers. The stock market has taken a bit of a reversal early in 2014. This is important for housing since much of the hot money is coming from excess funds from Wall Street and investors chasing yields like hungry hippos. The euphoria of a stock market juiced on Quantitative Easing has leaked into many areas outside of stocks including real estate once again. Yet the resulting re-inflation was largely based on investors cramping out regular home buyers. Regular buyers unlike the last bubble, are the last folks to the party. That is, the last bubble was because of too many regular buyers over stretching with toxic mortgage junk (and prime mortgages with weak income due diligence) while this cycle is because of Wall Street using easy money from uncle Fed. This is why the rise in adjustable rate mortgages (ARMs) and jumbo mortgages so late in the game tells you that families are simply unable to compete with big money and once again, are stretching out their budgets for as much as they can get. Many even with low rates cannot compete so they have taken the next alternative in the form of renting. One thesis I think largely being missed is that the real estate market has caught a ride on the coattails of the non-stop stock rise since 2009. Four years of stocks only going up with QE as a backstop have conditioned people to believing that stocks and real estate only go in one direction. What happens when the juice no longer holds the same kick as before?

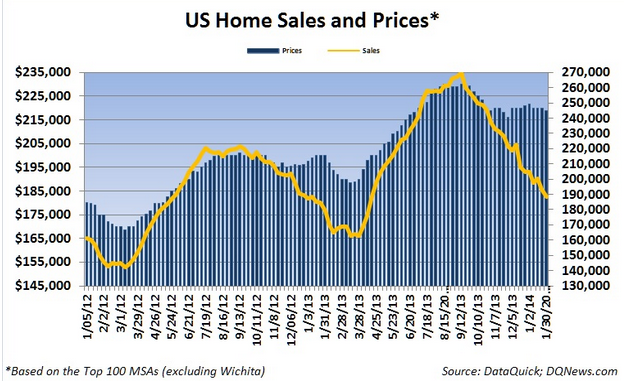

Prices and sales stalling out

Home prices and sales have hit a snag since the summer of 2013. Investors in many areas are actually pulling back since yields are no longer generous. There is only so much you can squeeze out of the public when incomes are not going up. Many younger Americans, the future home buyers, are essentially getting by on lower waged jobs and are deeply in debt with college loans. Many are living at home with mom and dad. Since the summer of 2013 the rise in interest rates with prices getting out of control has put a stop to the short-term QE induced investor mania. Investors have been purchasing close to 30 percent of all properties nationwide since 2009. That is simply unsustainable. There does appear to be some sort of slowdown approaching:

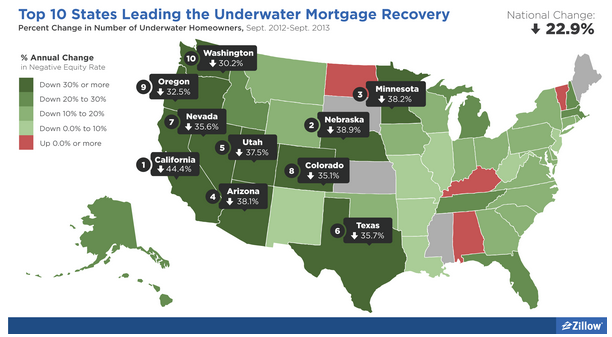

Sales have taken their usual seasonal hit and prices are stalling out. There is no way prices will rise this year similar to what we have seen. The notion is that prices will simply stall out for the year which is very likely. Depending on the stock market, they will likely have a year-over-year negative hit by the second half of the year. Inventory remains very low and you have millions of people in underwater properties still trying to get by paying their mortgages. Even with the fast rise in prices, we still have about 10 million homeowners across the country underwater:

What is interesting is that many of the distressed properties are now back in the hands of financial institutions. These financial institutions depend on a healthy stock market for a variety of business income. The recent stock correction, if this is something that is going to stick, will add additional fuel to the downside of a housing market that was already stalling out. After all, we have many of these big investors trying to sell their rental securitization streams on the stock market.

Sales in December for California were the slowest on record since the market implosion of 2007:

Beyond the massive drop in sales, this is important to note because it happened during a time when prices soared. Of course they soared on low inventory, massive investor buying, and regular buyers going manic by diving in with ARMs and jumbo mortgages. For places like California, a large part of the euphoria comes from booming markets. The rise in the stock market and sales has increased tax revenues, property taxes, and will result in solid capital gains. Yet these are fickle sources of income. What happens if there is even a modest correction in the stock market? Say stocks dip 10 or even 20 percent this year? What about home prices retrenching 5 to 10 percent? For a place like California based on non-stop growth, this can be enough to reverse things quickly. More than likely though, is we will continue to see a bi-furcation of the market where the majority of the state is pushed into theunaffordable crowd while those capturing most of the QE induced income gains will have the ability to leverage the low rate environment.

One quick lesson to take from this however is that real estate does change tides very slowly and the stock market can reverse very fast. It can also reverse on seemingly innocuous news but you would expect some kind of correction after going up by 150 percent from the lows in 2009 right? Yet some don’t bother to look at price-to-earnings ratios or even the fact that people can actually afford homes at current prices based on income. What is certain is the juice needs to keep coming for this to continue. So far, some of the juice is running out in 2014.

Do you think the stock market will have an impact on housing as a leading indicator?

via:http://www.doctorhousingbubble.com/housing-market-and-stock-market-stocks-impact-real-estate-as-leading-indicator/?utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+DrHousingBubble-HowILearnedToLoveSocal+%28Dr.+Housing+Bubble+-+How+I+learned+to+Love+SoCal%29

No comments:

Post a Comment